The Pending Divorce of Wind and Solar

The Pending Divorce of Wind and Solar

Wind is a dying industry. Solar is not.

This post has a simple point, so I’ll try to get straight to it. Because both wind and solar are subsidized, many of us who are pro-nuclear tend to put them into the same bucket. Pick your favorite term: ‘intermittent’, ‘weather-dependant’ or ‘variable renewable energy (VRE)’.

This misses something going on in the real word. Wind is a dying industry. Solar is not.

This seismic shift will improve the argument for nuclear — eventually. People ‘get’ the time-of-day, seasonal, and location limits on solar. Batteries will become nuclear’s competition for that rare resource—policy-maker headspace.

My field is the history of technology, especially innovative ones. Seeing technology trends is a tricky business. It’s easy to see what you want to see.

But I couldn’t help but see a trend in this chart posted on X on November 2 by Joshua D. Rhodes:

Anything on Twitter/X, of course, needs due diligence. But both Rhodes and the data check out. Rhodes holds a PhD in Civil Engineering from the University of Texas at Austin, where he is now a Research Associate. The data comes from filings at FERC, the Federal Energy Regulatory Commission.

Points at which trend lines cross are are always interesting in technology history. Rhodes, who seems to be personally in favor of both wind and solar, reposted this chart, evidently based on 2018 FERC data:

I thank Joshua Rhodes for the charts. But I draw a different conclusion, based on the histories of the two technologies. Wind is dying. Solar is not.

Infant no longer

The original justification for renewables subsidies was that innovation, learning effects and economies of scale would bring costs down.

Wind did have ‘infant industry’ learning period — in the 1980s and 1990s. But there was an inflection point in the early 2000s, after which the cost of wind started going up. Onshore wind has been a ‘mature’ technology for at least two decades.

Dr Gordon Hughes, a Professor of economics at the University of Edinburgh, has taken advantage of the fact that in the UK, special purpose vehicles (SPVs), used in that country to finance large wind projects, must publicly disclosure their financials.

In this chart, focus on the blue dots, which are from actual data for large UK windfarms. The overly-optimistic solid trend lines are from BloombergNEF and IRENA, the International Renewable Energy Agency:

Data from the US National Renewable Energy Laboratory (NREL) shows a similar 2003 inflection point:

The capital or so-called CapEx cost of wind projects includes the turbines (about 70%), site preparation, interconnection, and various soft costs, such as permitting.

Aside: High wind areas can be remote from population centers where the electricity is needed. It’s become a contentious accounting issue whether the cost of special transmission, such as Texas’ $6.9 billion CREZ line, should be included as a capital cost of the windfarms that benefit from them.

OpEx

But the history of wind technology shows its Achilles heel has been ‘OpEx’ — operating expenses, which include turbine repair and maintenance.

Turbines take a lot of beating from the wind. Their reliability deteriorates over time. Hughes’s UK data shows the odds that a typical onshore turbine will fail increases sharply after it has been in operation 10 years.

A quirk in the US tax code has ‘protected’ us from having to witness the infirmities of aging windmills. The production tax credit (PTC) for windfarms expires after 10 years. ‘Repowering’—replacing an old turbine with a new one—restarts the PTC clock. Given the perverse logic created by the subsidy, it’s cheaper to throw old turbines out.

In a recent repowering of a windfarm in San Gorgonio Pass near Palm Springs, the 23-year-old turbines were derided as antiques. Which they probably were. But most advocacy asserting the cheapness of wind power assumes turbines have a 25-year life. In the history, they have come nowhere close to that.

Wind has improved incrementally in the last two decades. This sort of steady, patient engineering work deserves credit in any field. It’s what took nuclear power plant capacity up into the 90 percents in the 1980s and 1990s.

Power ratings for newer turbines are considerably higher. One new one can replace a half-dozen old ones. The new turbines are better in low wind, and thus generate electricity more of the time. The blades spin more slowly, reducing noise and wear. And makes them less likely to kill birds.

A laudable wind industry innovation is IdentiFlight, an AI camera system that attempts to identify birds as they approach, although I have no idea how well it actually works. In theory, the IdentiFlight system sends a shutdown message to the turbines in time to protect approaching birds:

But these incremental improvements won’t be enough to save the wind industry—my reasoning to come.

Miners of the code

While wind turbine technology is interesting, but the wind industry has always been about mining the tax code. The renewables lobby includes not just the usual NGO suspects, but more politically significantly the Wall Street banks, which have made ‘tax-equity’ finance a speciality.

In 2003, James Dehlsen, the founder Zond, an early wind turbine company acquired in 1997 by Enron, was interviewed for a project documenting the history of wind in California. Dehlsen made this interesting observation: “In my view, the earliest breakthrough was not in technology, as would be expected, but the creation of a financial method for using the existing state and federal tax incentives for capital formation.”

A pioneer of innovation.

Offshore gigantism

In paleontology, there’s a conjecture that gigantism somehow seems to precede extinction.

Offshore is wind certainly becoming leviathan:

Turbine blades being loaded onto a ship in Hull, England:

And for context, the GE Halidade-X next to some well-known verticals:

Rough seas ahead

The Biden administration’s announced target is to build 30 gigawatts of offshore wind by 2030. At an (optimistic) capacity factor of 40%, this would produce 12 GW of electricity—at various times of the day and night.

The engineering challenges of such a quixotic project are enormous. The Atlantic is not the Thames Estuary or Dogger Bank, both of which are flat, shallow, and relatively protected from severe storms.

Both the first-of-a-kind engineering and cost range of $30-40 billion are in same ballpark as large nuclear. I think it’s best treated as a single, ill-advised megaproject.

Fortunately, at the moment it doesn’t seem likely to happen. “Offshore wind in the U.S. is fundamentally broken," Anja-Isabel Dotzenrath, BP's head of gas and low carbon, told a Financial Times conference on November 1st.

To recap the news from last few months:

On November 1, BP and its Equinor announced a combined $840m write-down related to their join Empire Wind 1 and 2 and Beacon Wind 1 wind farm projects off the coast of New York. In October, the New York Public Service Commission rejected petition by the companies to renegotiate the power purchase agreements for the projects. BP is the former British Petroleum; Equinor is based in Norway.

On November 1, Ørsted, the Danish company that is world’s largest offshore wind developer, said it would cease development of Ocean Wind 1 and 2 off New Jersey.

On Oct. 23, General Electric Wind Energy said its offshore-wind operations will post an annual losses of $1 billion for this year and another $1 billion in 2024.

Earlier in October, Siemens Gamesa, the wind-energy giant formed in 2017 by Siemens’ acquisition of Spanish rival Gamesa, sounded out the German government for a loan guarantee of €16 billion.

In October, Avangrid, a subsidiary of the Spanish utility Iberdrola, cancelled the power purchase agreement it had with Connecticut for the Park City offshore wind project, following upon another cancelled agreement with the state of Massachusetts for the South Coast project.

In July, Vestas Wind Systems, the world’s largest maker of turbines, reported a loss of 147 million euros (about $151 million) for its third quarter. Henrik Andersen, its chief executive, said in an interview, “Every time we sell a turbine, we lose 8 percent.”

A lesson from history

Wind—onshore—went one through a ‘bigger is better’ technology phase in the 1980s. It did not end well.

For a wind single turbine, there are three ways to increase output:

Put it in a windier location.

Increase its height. The rule of thumb is that if you increase the height of the hub by x, wind speed up there increases 14% of x.

Increase the diameter of the rotor. Power increases by the square; thus doubling the size of the rotor increases power production by 4 times.

The aerospace engineers who designed the first generation of US wind turbines pushed these to the max. More power would be more economic, right?

The resulting designs promptly self-destructed in real-world wind conditions. The clunky, inelegant Danish wind turbines, which had evolved from farm equipment, proved far more reliable. They quickly took over the US market.

Offshore turbines operate 24/7 in an extremely hostile environment. To fix them, you have to send somebody out in a boat. Gordon Hughes’s UK data shows OpEx costs for offshore windfarms are far higher than for onshore.

The value proposition, illustrated

I’ve become addicted to GridBrief’s weekly “What’s Keeping the Lights On?” charts, which GridBrief collects off the EIA website.

In this one for California, I believe we see the near-future of the grid in the western United States and Texas:

There are large peaks of solar during the daylight hours. Natural gas, of course, dominates overall. More natural gas, from peaker plants, comes on at sundown, and, to a lesser extent, before sunrise. Hydro, interestingly, is also used for peaking on the evening shoulder. Batteries charge during the day — that’s where the gray line is below zero — and also come in at the shoulder. But they don’t last very long.

Wind is a kind of scribble along the bottom.

Diablo Canyon was evidently offline two days during that week in California, but in the charts for most ISOs, nuclear is a boring horizontal line.

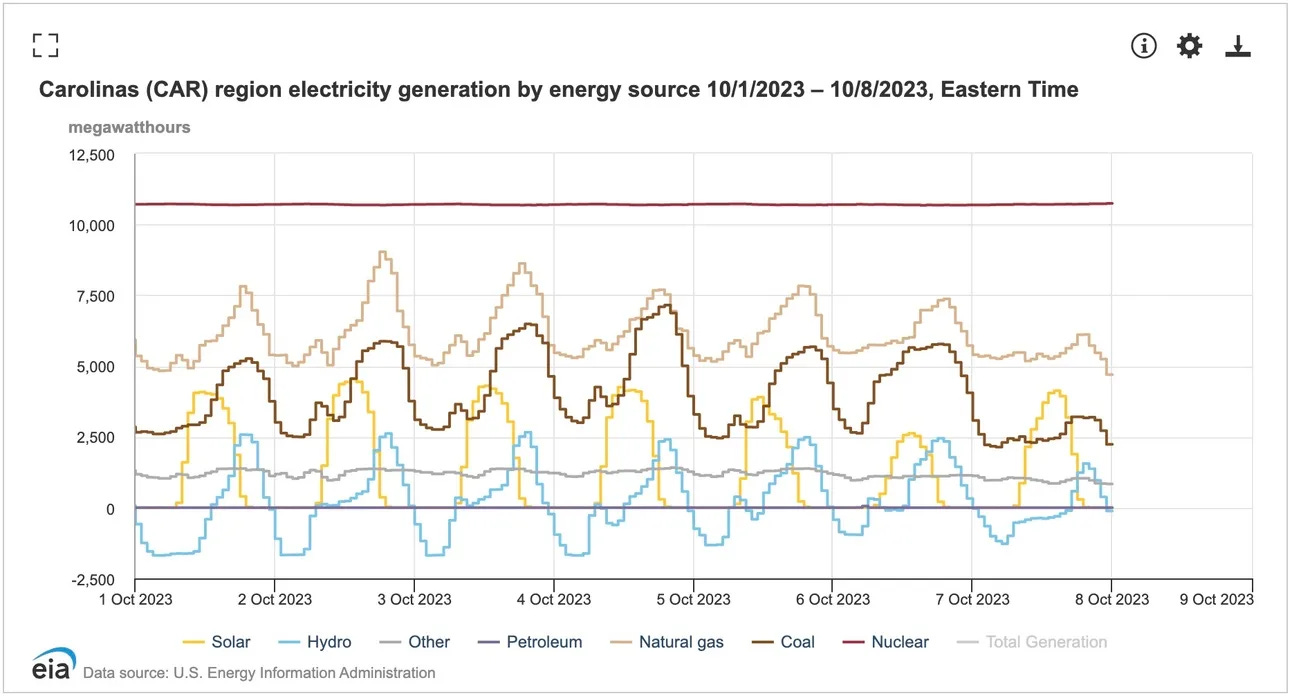

Boring, I might point out, is exactly what baseline ought to be. It would be nice to have a grid where you don’t have to accommodate everything else to renewables. The Carolinas have one:

But my point here is to show where wind fits in.

It doesn’t. It’s too erratic.

The economic value of any source of electricity comes from its ability to generate electricity when it is needed.

In California and Texas, during the summer, solar has economic value because it generates electricity when the air conditioners are on.

Economic value, or deficiency thereof, has always been the fundamental problem for wind. Incremental improvements in turbine technology will not be enough to overcome it.

What’s different now is that wind has serious competition from within its own ‘renewables space’.

Wind will become the ugly sister, outshined by solar.

Solar’s worst enemy — itself

It’s not all roses. Solar’s second victim will be itself.

But first, a recap of how solar got to where it is today.

There’s been an entire book written about How Solar Energy Became Cheap (Gregory F. Nemet, 2019). It’s expensive, but I recommend it.

To summarize, five decades of subsidies by a rotating cast of governments worked:

Electro-mechanical things made at scale enjoy cost reductions, but the function is basically linear. When a manufacturing process is akin to printing, as in semiconductors and solar panels, cost reduction curves are non-linear.

Exactly how cheap solar has become is difficult to say. PV modules themselves are now the cheapest source of bulk electricity around. But the modules need to be wired up, permitted, installed, and so on.

Which does not mean the solar panel industry is in perfect health. On the contrary, it’s experiencing a syndrome familiar who has followed the semiconductor industry: ‘profitless prosperity’.

Solar panels have become a commodity. Competition among the five Chinese firms that make them has been ruthless, driving down margins. That’s the ‘profitless’ part.

There’s currently an oversupply of panels. It’s a buyer’s market. That’s the ‘prosperity’. In July 2023, 40GWdc of Chinese-made of panels were reported sitting in warehouses in Europe awaiting installation, according to RystadEnergy.

In the US, a lot of solar is going to get installed in the next few years. Estimates based on what’s in the connection queues must be taken with a pinch of salt (it doesn’t all get built), but Lawrence Berkeley Lab reports that at the end of 2022, there was 947 GW of utility-scale solar power capacity in the interconnection queues, 456 GW of which include batteries. Compare with the proposed 30 GW from offshore wind.

But the amount of solar a grid can take is inherently self-limiting.

This results from a phenomenon known to the pundits as value deflation. It’s pretty simple: there are only so many hours of sunlight per day. Once a lot of solar is being generated during them, additional solar is not worth very much.

Solar will cannibalize itself. The next subsidy battle will be over batteries, needed to save solar from itself.

For policy wonks only

I’m at the length limit, so I’ll keep my “What is to be Done?” short.

Solar can’t be stopped, even if the subsidies are ended. Which they should be, since they are unnecessary. The rentiers of the green economy will howl, but let them.

For existing onshore wind: end the subsidies and declare Mission Accomplished. We’ve done our bit for wind. In places where wind resources are good and transmission already built, wind might viable. Let the market sort that out.

The public-policy nightmare to avoid is wind becoming a permanently subsidized zombie technology, comparable to corn ethanol.

The 1980s California wind rush of the ended abruptly when the Reagan administration passed the Tax Reform Act of 1986. I don’t see that happening if the PTC is ended today, but instead see wind devolving over a few decades into a niche energy source. The profitability of the windfarms that survive the shakeout will go up and down with the price of natural gas.

Batteries will be the new darling infant technology. A subject for a future post.

In the dance for the public purse, some participants will change partners. Instead of ‘wind and solar’, get used to hearing ‘solar and storage’.

As solar becomes more dominant, nuclear might consider what I call the sneaky Cuckoo’s Nest strategy: gain public acceptance as the necessary supplement for solar. Nuclear works at night, in the winter, and in parts of the country where the sun don’t shine. Once it gets built, it will finally occur to someone, “Why don’t we just leave the reactor on all the time?”

In terms of innovation, solar and batteries have yet to exhaust their possibilities. Polysilicon panels are only one technology. Flexible, printable, and transparent solar is possible. The best US counter to China’s dominance is not tariffs, but to invest in solar R&D: try to invent to the next generation; then, if we do, nurture and hang onto it for a change.

A last word about nuclear. A trenchant observation (I think) about SMRs is that they are a nuclear engineering solution to a financial engineering problem. The wind industry played the financial engineering game with consummate skill. That part of the history might be worthy of some study.